library(xts)

library(gdata)

library(ggplot2)

library(grid)

library(quantmod)

library(ggthemes)

load(url("http://statrstart.github.io/data/d2010_2015.RData"))

temp <- tempfile()

download.file("http://www3.boj.or.jp/market/jp/etfreit.zip",temp)

con <- unzip(temp, "2016.xls")

d2016 <- read.xls(con,header=F,skip=8)

unlink(temp)

d2016<-d2016[,2:4]

names(d2016)<-c("date","ETF","REIT")

d2016$ETF[is.na(d2016$ETF)]<-0

d2016$REIT[is.na(d2016$REIT)]<-0

d2010_2016<-rbind(d2010_2015,d2016)

x <- read.zoo(d2010_2016)

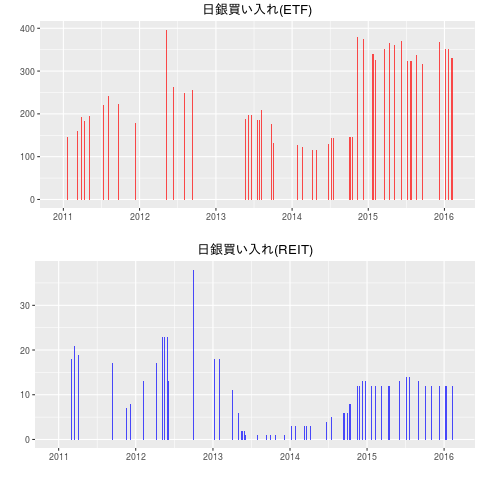

a<-ggplot(data = fortify(x[,1], melt = TRUE),aes(x = Index, y = Value) ) +

geom_bar(stat="identity",position=position_dodge(),fill=rgb(1,0,0,alpha=0.7)) +

labs(title="日銀買い入れ(ETF)", x="", y="")

b<-ggplot(data = fortify(x[,2], melt = TRUE),aes(x = Index, y = Value) ) +

geom_bar(stat="identity",position=position_dodge(),fill=rgb(0,0,1,alpha=0.7)) +

labs(title="日銀買い入れ(REIT)", x="", y="")

grid.newpage()

pushViewport(viewport(layout=grid.layout(2, 1)))

print(a, vp=viewport(layout.pos.row=1))

print(b, vp=viewport(layout.pos.row=2))